I come from a family of educators; my husband from a family of entrepreneurs. This can make for interesting fodder at family get-togethers. Some conversations are funny, others are uncomfortable, but one such conversation piqued my interest. The discussion centered around “earned income potential” and teachers’ strategic position to boost this potential.

I started thinking…as an educator, when is the best time to invest in your career? How much can a lane change (or two) boost potential earnings?

I spent the last couple months collecting and analyzing teacher salary schedules from across the nation. I examined the scales, crunched the numbers, and created the following examples (so you don’t have to!). The results were clear.

No matter how many years of teaching you have under your belt, you should consider investing now. Here’s why:

New Teachers

If you want to increase your lifetime earning potential, you should try to earn as much as you can as quickly as you can, right? It may surprise you to learn how much difference a “lane change” can make over time.

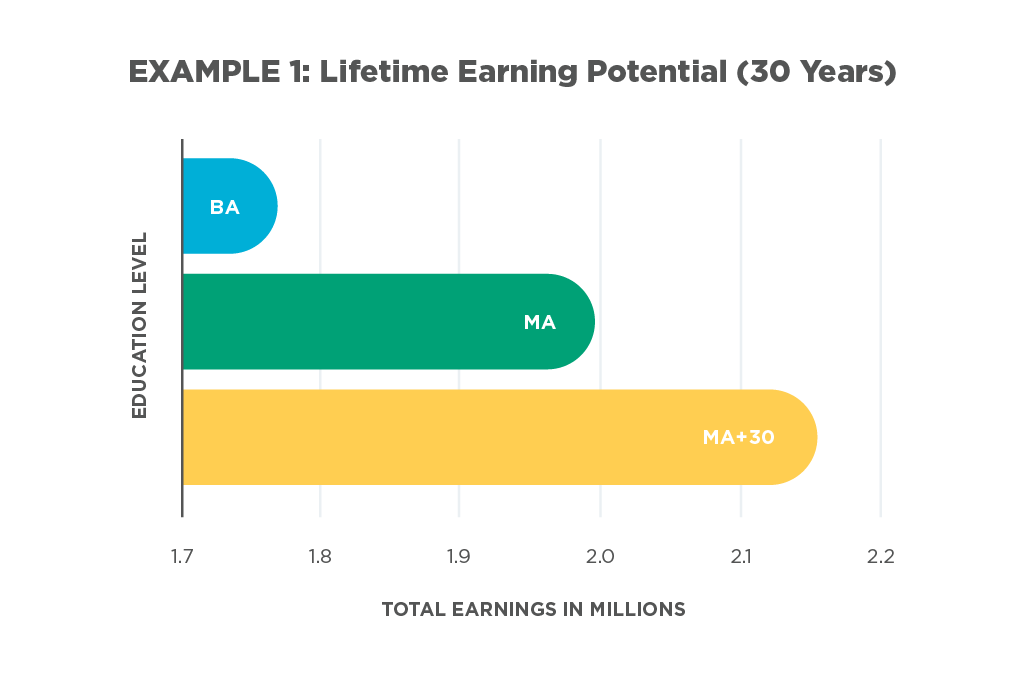

Example 1 (below) demonstrates the potential impact of earning your MA and your MA + 30 over a 30-year career.

You can make millions in education! Note the percentages of growth in this data, applied from a teaching schedule on the East Coast. Based on this example, it is possible to increase your lifetime earning potential by 10% if you complete your master’s degree within 5 years of your career, and 20% if you complete your MA + 30 within 10 years. That is an incredible increase!

Quick Tip: New teachers should also be leery of what I call the ” holding pattern.” Many districts freeze teacher salaries in the early years (typically around years 3-9). This practice allows districts to entice new instructors with higher base salaries and keep a handle on teacher salaries overall. While I understand why districts do this, it hardly seems fair. If your salary schedule includes a “holding pattern” you could be teaching for 3-5 years (or 13% of your career!) with no real increase in salary. The only way to increase salary during a “holding pattern” is to earn those graduate credits and move horizontally into a new lane.

Seasoned Teachers

Anyone with 10 or more years of teaching experience falls into this category. At this point, you have most likely surpassed any “holding patterns”, and are looking at a decent, steady pay raise each year. This next sentence may be hard to swallow, but I will explain my logic below: This is the easiest time to invest in your career.

Although it may not seem like it initially, by investing your pay raise for one year into graduate credits, before you factor your raise into your budget, you can put that money to work and not “feel” a thing. Additionally, if you are able to move one lane within one year, you will be looking at a larger salary increase the following year… and every year thereafter! This is a great time to shoot for small horizontal moves such as an MA+9, MA +12, MA+18, etc.

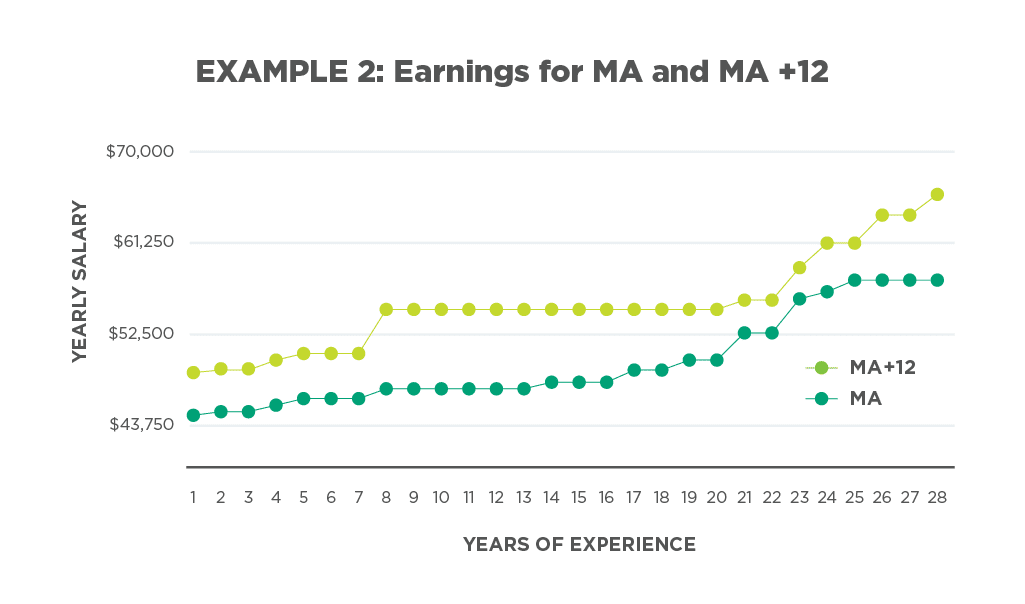

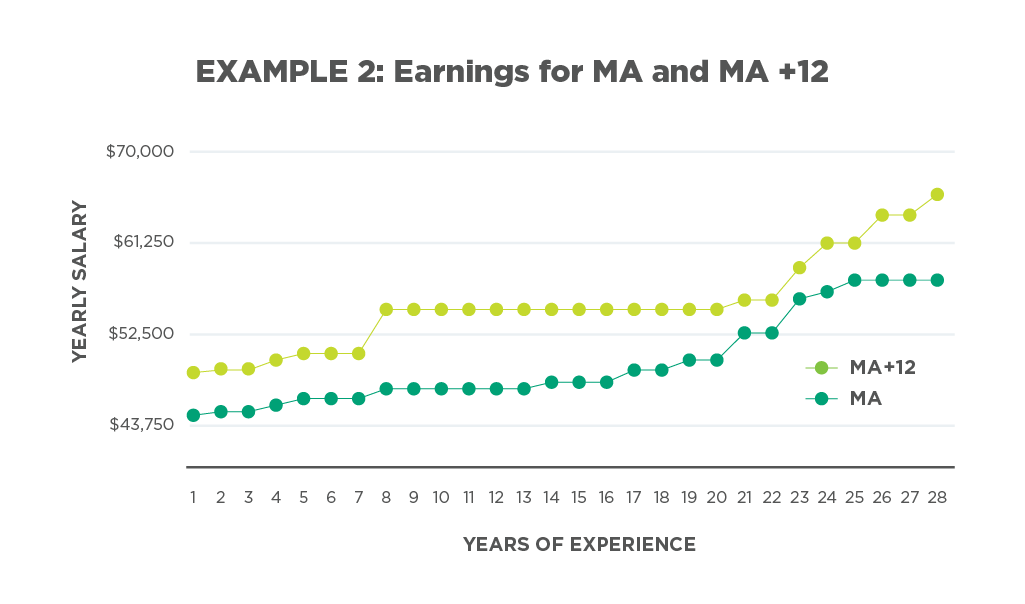

Example 2 (below) demonstrates how investing in your career will actually pay for itself the following year.

According to this graphic, with data from the Midwest, a move into the MA + 12 lane would increase teacher salary by $4000-7000 a year! To put this into perspective, consider the cost of earning an MA+12. At The Art of Education, graduate credits cost $399 per credit hour. This means earning your MA +12 would cost approximately $4788. According to Example 2, you could pay off your credits with one years’ salary increase (and have a little extra spending to boot!)

Quick Tip: Seasoned teachers should keep an eye out for maximized lane steps. In a nutshell, this means you have been in one lane for so long that the district caps your salary. Some districts offer longevity additions, but not always. If you have reached the end of your lane, the only way you can earn more money is to move horizontally into a new lane. Generally, the farther you move horizontally, the more steps there are in each lane. Investing enough to move one lane could buy you several more years of salary increases before you max out again.

Veteran Teachers

Veteran teachers are those considering retirement in the next 5 years. You might think at this point in your career, an investment in graduate credits is pointless. However, many retirement plans are calculated based on the last 3-5 years of earnings. If this is the case for your state or district, the salary you earn at the end of your career could determine the quality of living for the rest of your life!

Example 3 (below) demonstrates how lane changes affect monthly retirement earnings.

In this example, from the Southeast, it is clear that moving to that next lane can add several hundred dollars to your monthly budget. That might not seem like a whole lot of cash initially, but when you consider the duration of your retirement (pretty much forever!) it can really add up over time.

Quick Tip: The best advice at this point in your career is to seek out a retirement specialist in your district and ask questions – the sooner the better. The choices you make are pivotal and will impact you and your family for many years to come. Make sure to get the facts you need to retire at the top of your game!

Every pay scale is different, take the time to dust yours off and see how these examples might apply to your situation. I hope I have planted a seed to get you thinking about investing in yourself and your career. As it turns out, I can agree with my in-laws on this one. As educators, we have the ability to increase our net worth and we should take advantage of it! If you’re interested in learning more about graduate classes available at The Art of Ed, click here to visit the Classes page and here to visit the Studio Classes page.

What are your educational goals?

What level of education do you hope to achieve?

Magazine articles and podcasts are opinions of professional education contributors and do not necessarily represent the position of the Art of Education University (AOEU) or its academic offerings. Contributors use terms in the way they are most often talked about in the scope of their educational experiences.